Students are increasingly concerned about taking out student loans, and for good reason. The cost of college tuition has risen steadily in recent years, and you may be understandably concerned about taking on debt. If you have taken out a federal student loan or are considering taking one out, here’s what you need to know about disbursement and repayment.

Only Take What You Need

When you fill our your FAFSA, your college or university will offer you a financial aid package. This might include a combination of grants, work-study, scholarships, and loans. Apply for the first three, and only take the federal student loans you need. You can reduce or decline any award amount. Taking the maximum amount of loans, just because you can, will only result in more debt.

You won’t have to repay your loans as long as you’re in school full-time. This applies to graduate school and professional programs, as well. Keep in mind you may need to submit new documentation each year to prove your course of study.

Understanding Student Loan Repayment

Once you graduate, you should prepare to repay your student loans. The federal government offers a 6-month grace period after graduation before you start repayment. This is a good time to weigh the pros and cons of each repayment option and make a decision that works for your budget and current needs. Repayment options include:

- Income-based repayment options will allow you to make payments that are commensurate with your income. As you make more money, your payments will increase. The payment term can last up to 25 years. This may be a good option if your standard payments are more than you can afford, but keep in mind that interest will accrue during this time.

- Standard repayment allows you to pay off your loans over the course of up to10 years. Your first bill will tell you how much money to pay. Your payments should remain the same as long as you pay them.

- Graduated repayment begins with lower payments, but payments increase over time, usually every two years. These loans also are to be paid off within 10 years.

- Extended repayment allows you to pay your loan over a period of up to 25 years. Your payments may be fixed or increase over time. You must have at least $30,000 in student loans to be eligible for this plan.

- Revised pay as you earn creates payments that are no more than 10% of your discretionary income. Your payments are recalculated each year based on your income and family size. While your loans may be forgiven over time (after 25 years), you may have to pay income tax on the forgiven amount.

This is not an exhaustive list of repayment options. The federal government offers flexible payment options to fit any budget and financial goals. Keep in mind, with some of these plans you will have to pay more over time due to accrued interest.

State of the Student Loan Market

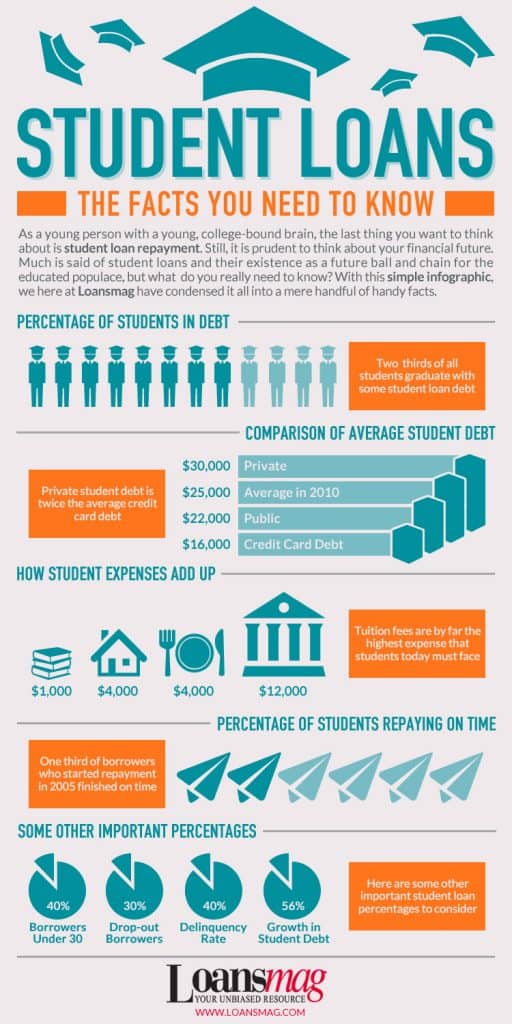

Check out this info graphic for an overview of the current state of student loan debt.

Understanding student loans is essential, especially when creating financial goals after college. Factor your maximum payment into your budget so you’re never in danger of missing a payment. A missed payment may result in wage garnishment, credit concerns, and other negative consequences. If you have any questions or concerns about repayment, talk to your student loan servicer.

Additional Resources:

https://studentaid.ed.gov/sa/repay-loans/understand

https://studentaid.ed.gov/sa/sites/default/files/your-federal-student-loans.pdf

https://www.forbes.com/sites/rent/2015/10/22/student-loan-debt-101/#51c413c5dabb

http://www.asa.org/student-loan-basics/

https://www.usnews.com/education/best-colleges/paying-for-college/articles/2015/03/25/take-4-steps-to-understand-student-loan-interest-rates

https://www.creditkarma.com/article/student-loans-101